Forum

Name : Arthur Time : 2 June 2017 20:30

-

Courses : ACCA Professional Examination Preparatory Programme - Strategic Business Reporting -

Content : IFRS 5 question A parent put a wholly-owned subsidiary for sale on 31 Mar 2017, the intention of sale was announced on 15 May 2017 and no buyer has been identified. If no buyer is found before 31 Mar 2018, the subsidiary would be discontinued. If the subsidiary is discontinued, the parent would retain the subsidiary's trademarks of $10m. Investment in subsidiary: $40m Fair value less cost of sale: $35m The financial year end date is 31 Mar 2017. Given the sale is not guaranteed, is it correct to use 10m as initial measurement?

Reply: Time : 04 June 2017 10:21

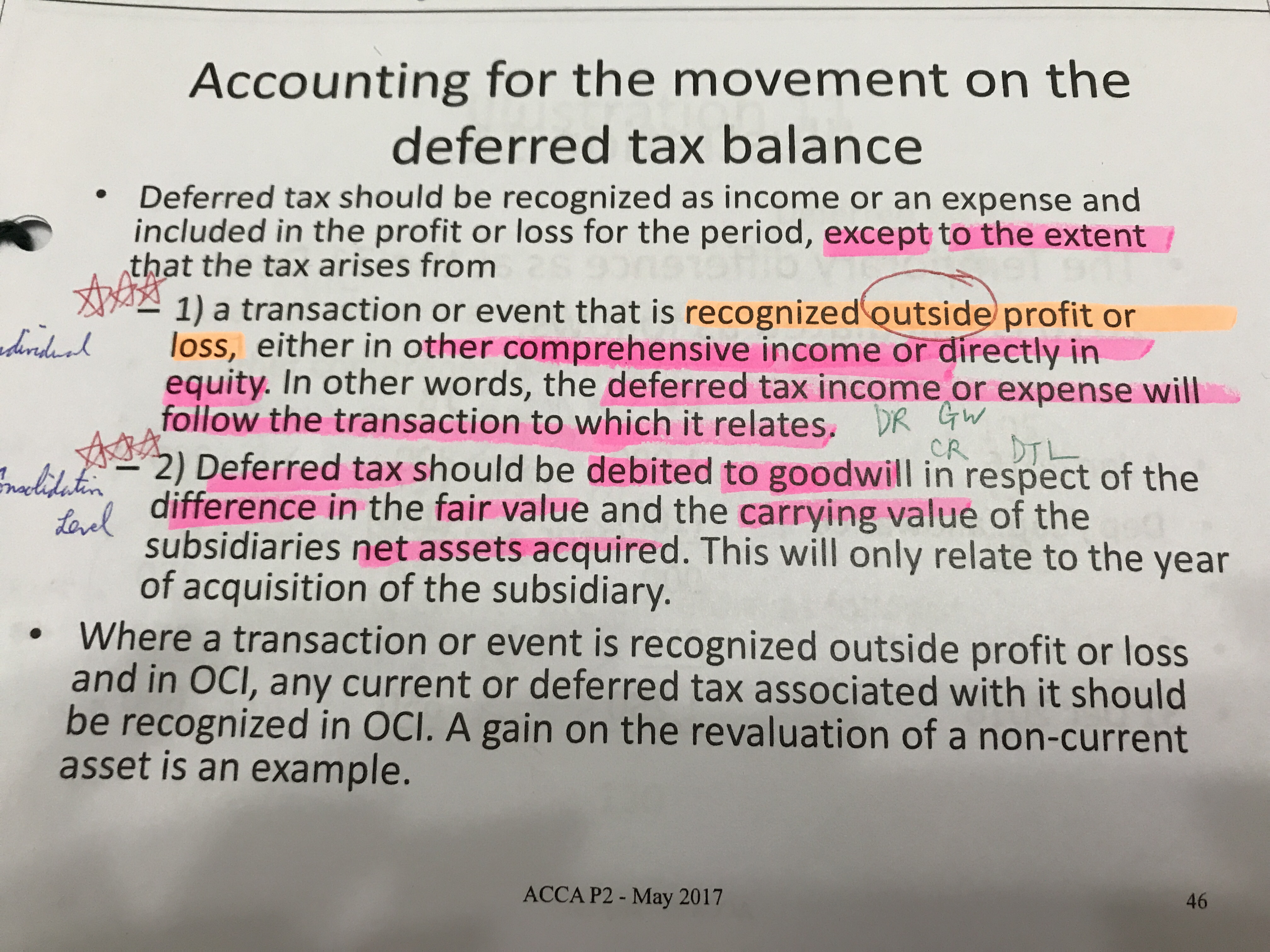

Name : Peony Time : 30 May 2017 19:59

-

Courses : ACCA Professional Examination Preparatory Programme - Strategic Business Reporting -

Content : Initial recognition of goodwill no deferred tax, why deferred tax should be debited to goodwill?

-

Document :  image.jpg

image.jpg

image.jpg

image.jpgReply: Time : 31 May 2017 00:04

Name : Peony Time : 30 May 2017 13:42

-

Courses : ACCA Professional Examination Preparatory Programme - Strategic Business Reporting -

Content : Per Dec 2015 Q1, exchange loss 4.6 go to NCI, 7 go to where? I can't find it in the workings.

-

Document : image.jpg

Reply: Time : 30 May 2017 23:58

Name : Peony Time : 27 May 2017 17:06

-

Courses : ACCA Professional Examination Preparatory Programme - Strategic Business Reporting -

Content : Per Dec 2012 Q1, dividend received from associate should be eliminated in group level, why answer presented as below: OCE Dividend income to RE (2m) RE Dividend income fm OCE 2m Puttin: share of post-acq profit 4.5-2m The final effect still eliminated 2m, why do so much transactions?

Reply: Time : 29 May 2017 09:34

Name : Peony Time : 26 May 2017 16:45

-

Courses : ACCA Professional Examination Preparatory Programme - Strategic Business Reporting -

Content : June 2014, l can't find the figure of revaluation surplus $5.

-

Document : image.jpg

Reply: Time : 27 May 2017 12:15

Name : Peony Time : 24 May 2017 20:34

-

Courses : ACCA Professional Examination Preparatory Programme - Strategic Business Reporting -

Content : Dec 2011 Q1, I don't understand the corridor approach and how to measure asset ceiling.

-

Document : image.jpg

Reply: Time : 26 May 2017 11:34

Name : Peony Time : 25 May 2017 00:32

-

Courses : ACCA Professional Examination Preparatory Programme - Strategic Business Reporting -

Content : Per Dec 2011, GW impairment of Captive using 80% of Traveler's share, but per June 2013, GW impairment of Park using the amount of $53.3, I am confused that which situation using percentage or actual figure to calculate.

-

Document : image.jpg

Reply: Time : 26 May 2017 11:27

Name : Peony Time : 24 May 2017 13:10

-

Courses : ACCA Professional Examination Preparatory Programme - Strategic Business Reporting -

Content : June 2015 Q1, why investment in House $42 should be divided into 2 figures $20m & $22m?

-

Document : image.jpg

Reply: Time : 24 May 2017 17:51

Name : Amy Time : 1 May 2017 12:05

-

Courses : ACCA Professional Examination Preparatory Programme - Strategic Business Reporting -

Content : In jun 15 Q1-kutchen The answer use the expect value (5m shares x $2 x 20%) as contingent consideration. It let me confuse whether to consider the probability to fulfil the specified future conditions are met

-

Document : IMG2731.JPG

IMG2731.JPG

IMG2731.JPGReply: Time : 03 May 2017 11:23

Name : Amy Time : 22 April 2017 16:41

-

Courses : ACCA Professional Examination Preparatory Programme - Strategic Business Reporting -

Content : In notes on 5 Feb 17 consolidated financial statements (complex) - illustration 2 - full goodwill method Question state fair value of NCI ⋯ group policy to NCI using the full goodwill method. But in NCI working using the NCI % share of A & B ltd's net assets at date of consolidation.(it likely a partial goodwill)